The bank failures are coming fast and furious (and large)

now – a poor blawger can barely keep up. In my last post on bank failures, Bank

Failures Update And Future Problem Banks, I noted that the total number of

FDIC bank closures for the year was at 72, putting us on pace for an estimated

125-150 FDIC bank closures for 2009.

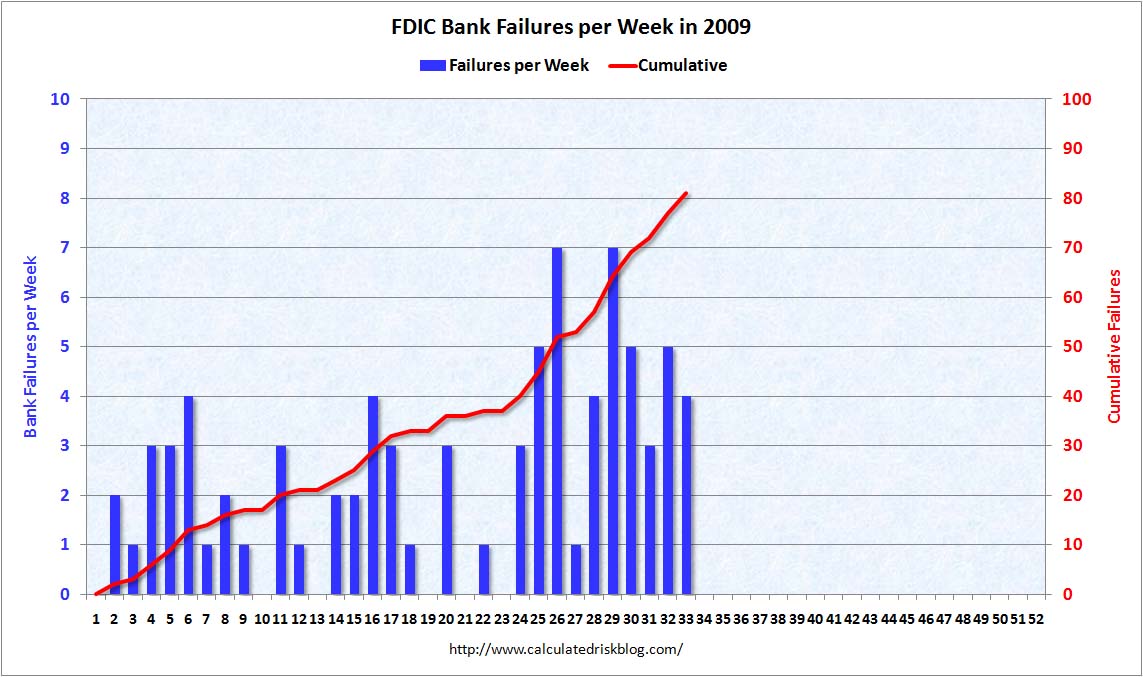

Since then, the FDIC has closed nine more banks, bringing

Since then, the FDIC has closed nine more banks, bringing

the total for 2009 to 81. See here

for the FDIC's full list of failed banks since October 1, 2000. The FDIC

has been seizing about 4 to 5 banks per week recently, putting us on pace for close to 150 bank failures for 2009. See the chart at right, courtesy of Calculated

Risk. (Click on any chart to

enlarge.)

Richard

Bove, a prominent banking analyst, predicts that "perhaps another 150

to 200 banks will fail," on top of the 81 so far in 2009, adding stress to

the FDIC's deposit insurance fund.

In the video below, Meredith Whitney predicts that, improved economic

fundamentals notwithstanding, we are still early in the bank failures cycle,

and will see bank failures top 300 before the end of this cycle (which Calculated

Risk believes is too low an estimate).

The current pace of bank failures is causing some strain to

the FDICs deposit insurance fund and to the financial system as a whole. From Reuters:

Richard Bove of Rochdale Securities

said this will likely force the FDIC, which insures deposits, to turn

increasingly to non-U.S. banks and private equity funds to shore up the banking

system.

"The difficulty at the moment is

finding enough healthy banks to buy the failing banks," Bove wrote.

The FDIC is expected on August 26 to

vote on relaxed guidelines for private equity firms to invest in failed banks,

after critics said previously proposed rules were too harsh and would actually

dissuade firms from making investments. . . .

Three large failures this year —

BankUnited Financial Corp in May, and Colonial BancGroup Inc, Guaranty

Financial Group Inc in August — collectively cost the fund roughly $10.7

billion.

The fund had $13 billion at the end of

March.

Regulators closed Guaranty's banking

unit on Friday and sold assets of the Texas-based lender to Banco Bilbao

Vizcaya Argentaria SA. The FDIC agreed to share in losses with the Spanish

bank.

Bove said the FDIC will likely levy

special assessments against banks in the fourth quarter of this year and second

quarter of 2010.

He said these assessments could total

$11 billion in 2010, on top of the same amount of regular assessments.

"FDIC premiums could be 25 percent of the industry's pretax income,"

he wrote.

This second graph from Calculated Risk shows the cumulative

This second graph from Calculated Risk shows the cumulative

estimated losses to the FDIC Deposit Insurance Fund (DIF) and the quarterly

assets of the DIF (as reported by the FDIC). (The FDIC takes reserves against future losses in the DIF,

and collects fees and special assessments – so you can't just subtract

estimated losses from assets to determine the assets remaining in the DIF.)

In a prior post, Bank

Failures in Historical Perspective, I compared the current pace of bank

failures to the pace during the S&L crisis and the great depression. At the current rate, bank failures in

2009 will outpace the early years of the S&L crisis. From 1982 thorough

1984 there were about 100 failures per year. After that, the number of failures rapidly increased, as shown

in this third graph, also from Calculated

Risk.

As the chart demonstrates, bank closures were far more

As the chart demonstrates, bank closures were far more

numerous during both the Savings & Loan Crisis and during the 1920s and

early 1930s, before the FDIC was created in 1933. For example, the number of bank failures is estimated at

4000 for the year 1933, and 500 bank failures per year was commonly seen during

the 1920’s. As I’ve noted in prior

posts, the number of bank failures alone does not tell the whole story of

distress from bank failures, which is a function of the total number of existing

banks, the size of their assets and liabilities, the number of branches, and

other factors. Nor do bank closures paint the whole picture of economic crisis

– in the current financial crisis, many of the most spectacular failures or

bailouts have been of non-bank financial institutions.

To get at some of these questions, Calculated Risk has a List

of Failed Banks since 2007, which includes assets and estimated losses. Finally, for those wanting a peek into

the future, see this unofficial List

of Problem Banks.

Related Posts:

Bank

Failures Update and Future Problem Banks

Kind of hard for me to look at some of those graphs and think that we're not running up into another Great Depressionary period. Which is one of the reasons I'm doing all I can to get out of debt asap. Looking too at precious metals.