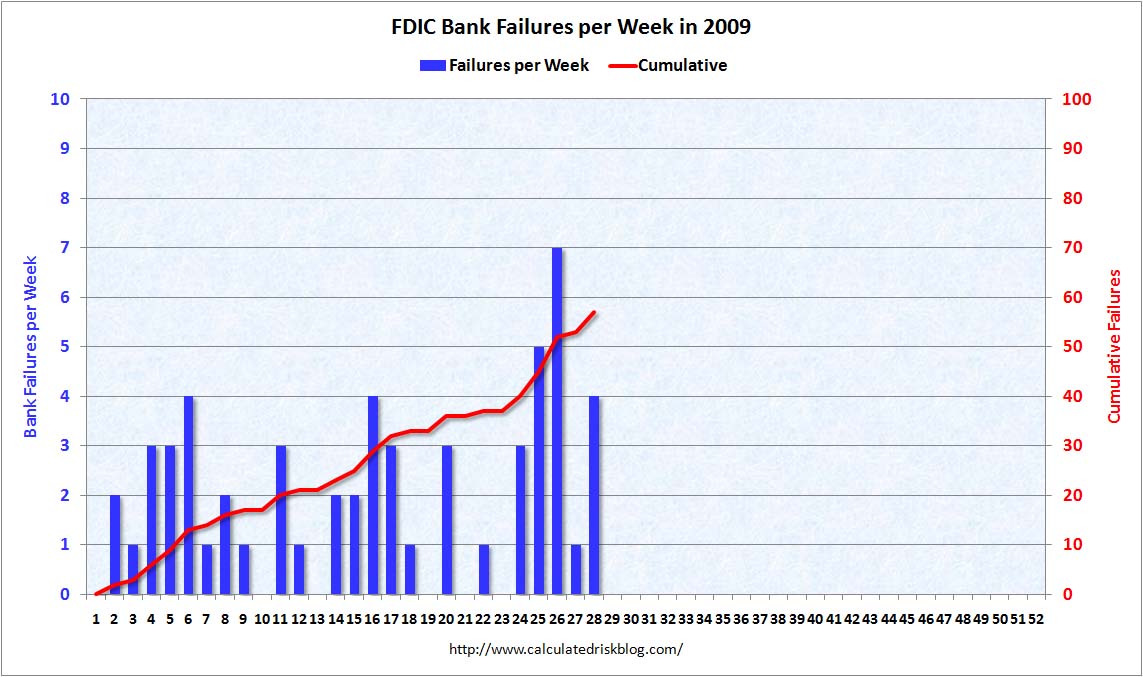

Calculated

Risk had a great analysis of bank failures over the weekend. On Friday, the FDIC closed four banks

— Temecula

Valley Bank, Temecula, California; Vineyard Bank,

National Association, Rancho Cucamonga, California; BankFirst,

Sioux Falls, South Dakota; and First Piedmont

Bank, Winder, Georgia – bringing the total number of FDIC bank closures for

the year to 57. See here for the FDIC's full list of failed banks since October 1, 2000. If the pace continues, we’re on track for close to 100 FDIC

bank closures for 2009 (See Chart 1 at right). (Click on charts to enlarge them)

Although that’s not a number to feel good about, it’s

helpful to put today’s FDIC closures in historical perspective. As shown in CR’s next chart (below), which

covers the entire FDIC period (1934 to present) bank closures were far more

numerous during the Savings & Loan Crisis. There were 28 weeks during which regulators closed 10 or more

banks. During 7 of those weeks,

there were more than 30 closures, and “the peak was April 20, 1989, with 60

bank closures.” (There was some

multiple counting during this period, but CR puts the effect as minor).

However, this third graph below (note the changed y-axis) includes

the 1920s, before the FDIC was created.

The number of bank failures is estimated at 4000 for the year 1933. In fact, 500 bank failures per year was

commonly seen during the 1920’s, and depositors typically lost 30% to 40% of

their deposits in the failed institutions.

As CR notes, the number of

banks isn't the only relevant measure of distress from bank closures. Many banks

today have more branches, and far more assets and deposits. Nor do bank closures paint the whole

picture of economic crisis – in the current financial crisis, many of the most

spectacular failures or bailouts have been of non-bank financial

institutions.

See Calculated Risk for more and for links to the source of

the FDIC and pre-FDIC data.

Nor do bank closures paint the whole picture of economic crisis – in the current financial crisis, many of the most spectacular failures or bailouts have been of non-bank financial institutions.

In addition to raw number of banks, it'd be great to see (failed deposits)/(total deposits) in order to get an idea of true magnitude.

It would Craig. Perhaps the FDIC deposit fund and reserve numbers provide some insight here? In short, I think a variety of relevant measures beyond the number of FDIC closures are available, but aren't as up to date or widely-accessible as the failed institution count. FYI — the pace of failures has accelerated in the past few weeks. The new estimate is 125-150 failures for 2009.